Budget

Proposed Seven-Year Budget

This proposal presents a conceptual seven‑year starting budget for the City of Green Valley. It is not authoritative. The first elected city council will adopt the actual budget, and it will be up to voters to choose representatives who reflect our community’s values and can distinguish between needs, wants, and desires when funding our city.

Our approach is intentionally conservative. We adjust figures as new information becomes available, rely on lower revenue estimates than we believe are realistic, and use higher‑than‑necessary expense assumptions in several categories. We would rather under‑promise and over‑deliver, recognizing that real‑world conditions will ultimately shape outcomes.

Key Points

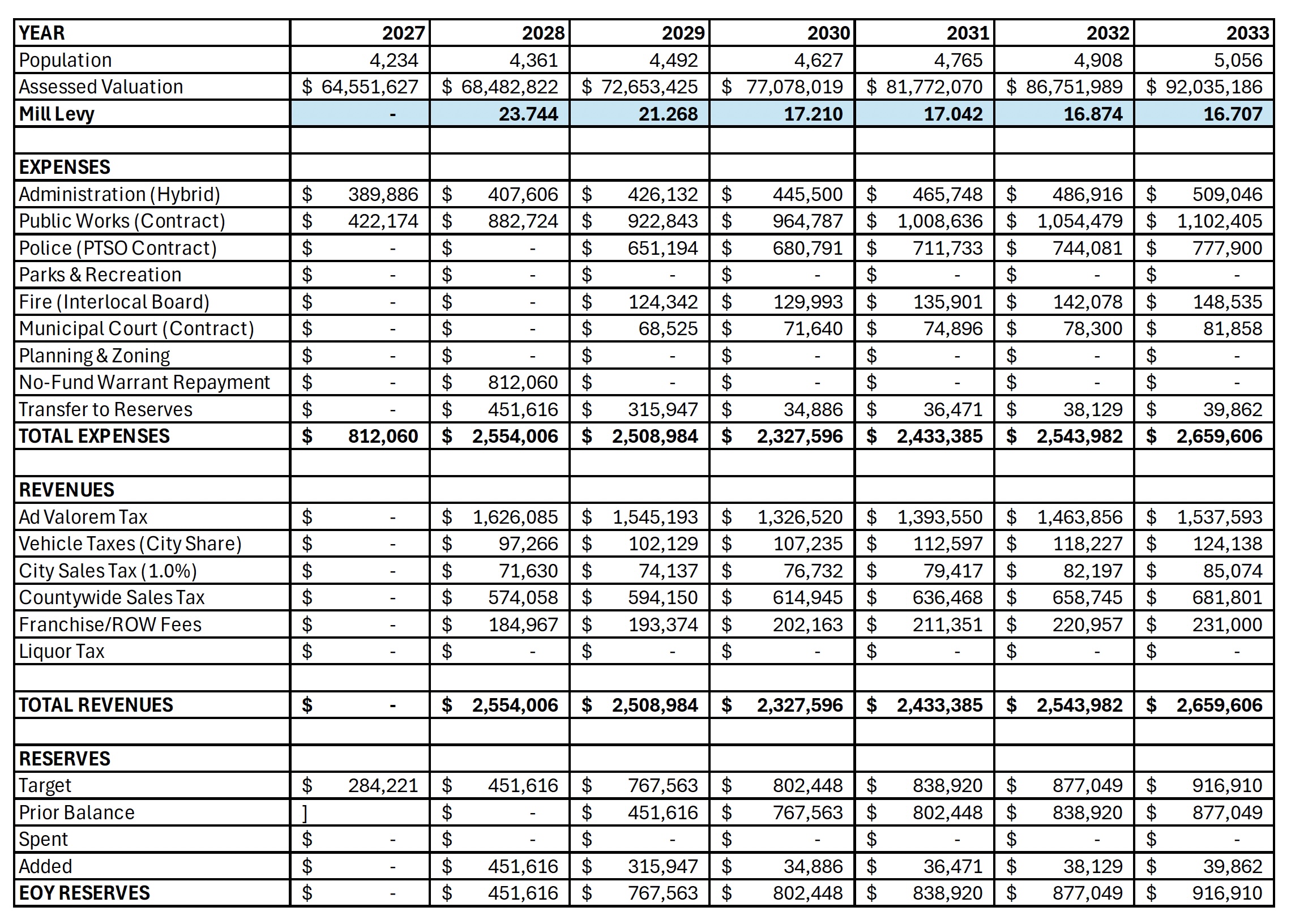

- FY27 has no revenue and no tax levies, because the city will not yet have a budget.

- All FY27 operating expenses will be paid using no‑fund warrants, which must be repaid in full in FY28.

- We assume six months of Public Works operations and expenses equivalent to a full year of Administrative operations in FY27, including startup costs and legal support.

- Valuation estimates use adjusted 2024 numbers, increased by 6.09% to approximate 2025 values. Actual valuation is likely higher.

- The city should provide only essential services in FY28 to repay FY27 warrants and establish responsible reserves. FY28, therefore, becomes the highest tax year, with an estimated 23.744 mills (a net increase of 15.263 mills).

- Contracting for police, fire, and municipal court services begins in FY29.

Service Level Multipliers

To estimate service costs, we used per‑capita averages from 12 comparably sized Kansas cities and applied multipliers appropriate to Green Valley’s startup conditions:

- Administration: 50% — A modern city should begin with minimal staff and rely on contracted support. Starting lean creates long-term pressure to remain lean.

- Public Works: 125% — We assume 25% higher spending than comparable cities to ensure realistic year‑round road maintenance. Contracting with local businesses avoids the cost of equipment, facilities, and permanent staff.

- Police: 50% — We anticipate contracting with the Pottawatomie County Sheriff’s Office for municipal code enforcement and enhanced patrols while preserving full budgetary autonomy for both the city and the county.

- Fire: 25% — Blue Township Rural Fire #5 remains in place. Through interlocal agreements with Blue Township Rural Fire #5 and Rural Water District #1, the city can provide targeted support that strengthens firefighting capacity.

- Municipal Court: 50% — Contracted judicial support is appropriate for a small city, and the municipal court should not become a revenue generator or major cost center.

- Parks & Recreation: $0 — Green Valley currently has no parks and does not anticipate collecting alcohol/liquor taxes that mandate recreational spending. Future councils may adjust this.

- Planning & Zoning: $0 — Initial staffing will be limited to a clerk, treasurer, and contracted attorney. Elected officials will rely on volunteer boards and contracted support during the city’s first decade.

Revenue Notes

- Ad valorem tax is calculated after accounting for all other revenue sources, consistent with Kansas municipal budgeting.

- Vehicle tax estimates use Wamego’s 2024 numbers, adjusted for 6.09% growth and inflation, with a conservative 5% annual growth assumption.

- Sales tax assumes a 1% citywide rate beginning in 2028. We estimate:

- ~$1.3M in Amazon deliveries

- ~$1.3M in other delivered goods

- ~$2M in physical retail

- ~$2.5M in construction materials

These are deliberately low estimates, increased only 3.5% annually to avoid overly optimistic ad valorem projections.

- Franchise fees assume 5% for telecom and gas, and 2.5% for electric utilities, anticipating negotiations with Evergy for city street lighting. Growth is estimated at 4.545%, using the efficiency factor rather than 6.09%.

- Countywide sales tax is estimated at 50% of Wamego’s numbers, significantly lower than figures suggested by a county commissioner in the previous hearing. We again use the conservative 3.5% growth factor.

- Liquor tax is not anticipated due to low revenue and administrative burdens.

Cash Reserves

Cash reserves are essential for financial stability and future bonding capacity. This budget begins building 35% reserves—enough for roughly four months of operating expenses, starting in FY28.

- Reserve targets increase annually to maintain the 35% ratio as expenses grow.

- FY28 and FY29 require the largest transfers due to startup conditions.

- FY30 and beyond require only modest increases.

Alternate Reserve Strategy

The first city council could adopt a phased reserve approach:

- 17% in FY28–FY29

- 25% in FY30

- 35% in FY31 and beyond

This would flatten the mill levy to 18.714, 20.477, 19.451, and 19.846 in those years, respectively. FY32 and FY33 remain 16.874 and 16.707 under either approach. The tradeoff is slower attainment of top-tier bond ratings.

Other Important Notes

- We assume 3% annual growth and 3% annual inflation, yielding 6.09% compounded increases in assessed valuation and service/material costs.

- Actual inflation, growth, and valuation changes will vary.

- Most services scale at a 1.5% efficiency rate, meaning costs grow at 4.545% compounded rather than the full 6.09%.

- For simplicity, we assume only residential growth and do not include commercial or industrial development, both of which would make the budget more favorable for families.

- All numbers are presented in a way that allows residents to verify the math and model their own scenarios.

- We intentionally use conservative assumptions to avoid presenting an overly optimistic picture.